![regional air travel in UK [Source Manufacturing Outlook]](https://autojournal.africa/wp-content/uploads/2025/11/regional-air-travel-in-UK-Source-Manufacturing-Outlook.png)

While the UK’s airports report record passenger numbers, the reality for regional air travel tells a far more concerning story.

Communities outside London and the South East increasingly rely on fragile air connections, which are under pressure from rising operational costs, environmental policies, and the collapse of key regional airlines. The domestic aviation network is shrinking, creating what experts call an “air gap” that threatens economic connectivity and regional equality.

Here are eight crucial facts and figures that illustrate the fragile state of UK regional aviation in 2025:

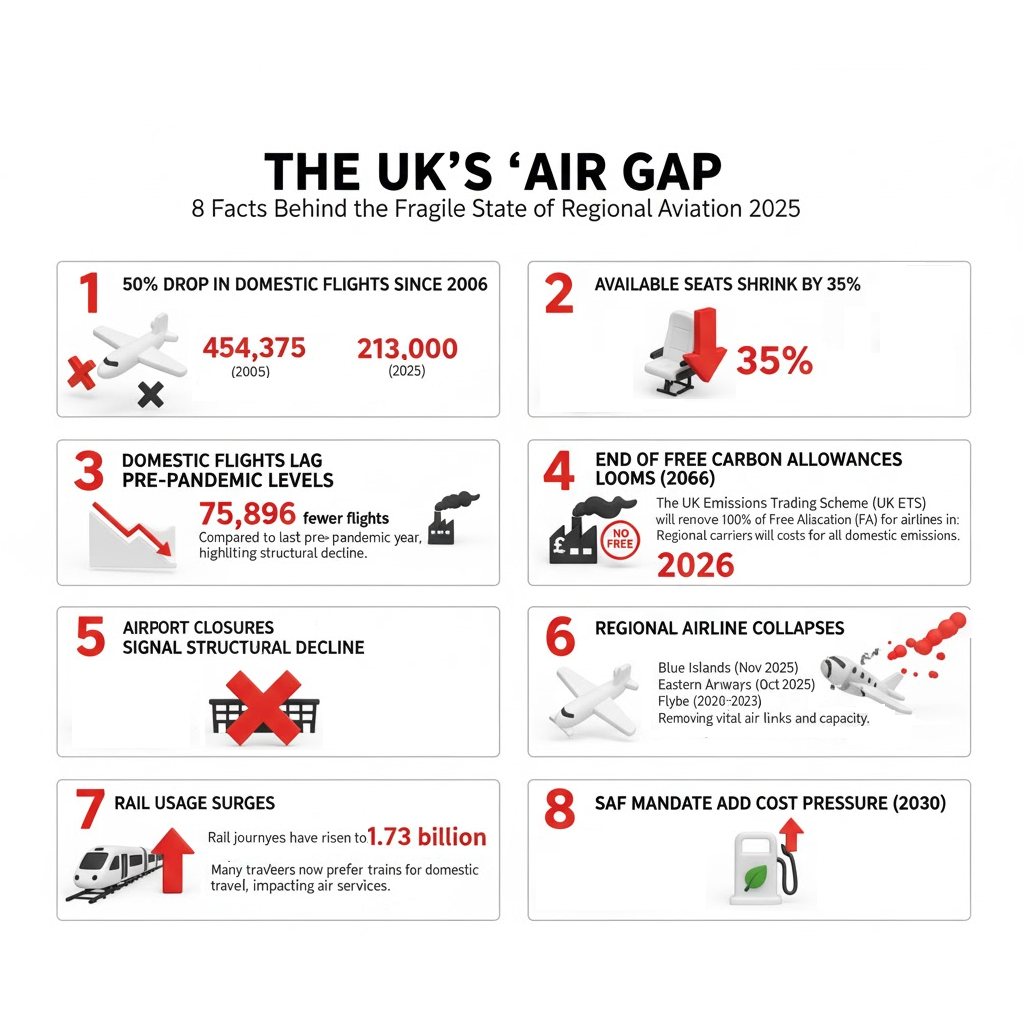

1. Domestic flights have halved since 2006

Scheduled domestic flights in the UK have fallen from 454,375 in 2006 to just 213,000 in 2025, representing a 50% reduction. This drop has caused the disappearance of many direct city-to-city links, leaving some communities dependent on slower or more expensive alternatives.

2. Available seats shrink by 35%

Domestic seat capacity has similarly fallen by 35%, dropping from 39.1 million in 2006 to 25.5 million in 2025. In practical terms, this reduction means more than 37,000 fewer passengers can fly within the UK every single day, further limiting options for business and leisure travellers alike.

3. Domestic flights still lag pre-pandemic levels

Even as international travel rebounds strongly, the domestic market has not fully recovered. The 2025 schedule is down by 75,896 flights compared with the last pre-pandemic year, highlighting a long-term structural decline in internal air connectivity.

4. The end of free carbon allowances looms

The UK Emissions Trading Scheme (UK ETS) will remove all free carbon allowances for airlines in 2026. Regional carriers, which often operate on narrow profit margins, will be required to purchase credits for all domestic emissions. The additional costs threaten the financial viability of already marginal routes.

5. Airport closures signal structural decline

Regional hubs have closed as commercial operations have become unsustainable. Doncaster Sheffield (2022), Blackpool (2014), and Plymouth (2011) airports all ended passenger services in the past decade, reflecting the shrinking footprint of regional aviation outside major global gateways.

6. Regional airline collapses show fragility

The collapse of regional carriers has accelerated the decline. Blue Islands (Nov 2025), Eastern Airways (Oct 2025), and Flybe (2020/2023) all ceased operations, removing vital air links to cities like Exeter, Southampton, Aberdeen, and the Channel Islands. These failures leave communities with fewer options and create immediate gaps in connectivity.

7. Rail usage surges as competition grows

Passenger behaviour is shifting. Rail journeys in the UK have risen as at the end of March 2025 to 1.73 billion. Many travellers now prefer trains for domestic travel, seen as more affordable and environmentally friendly, further pressuring regional air services.

8. Sustainable Aviation Fuel (SAF) mandate adds cost pressure

The UK government’s SAF mandate requires at least 10% of jet fuel to be sustainable aviation fuel by 2030. Given SAF’s higher cost compared with traditional kerosene, compliance introduces substantial financial strain, especially on regional airlines that operate thin-margin, low-density routes.

Read more on UK auto industry falls 11.9% in toughest year since 1953

![Luxury Air Travel 2026 [OTAA]](https://autojournal.africa/wp-content/uploads/2026/06/Luxury-Air-Travel-2026-OTAA-350x250.png)

{kind=link}